VIEWS

RETAIL: New Insights Show Big Disconnect Between South African Psyche & Positive Purchase Behaviour

Recent Gauteng Business News

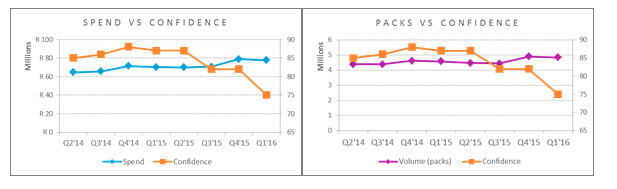

The fact that South Africa’s newly released Nielsen Consumer Confidence Index (CCI) figure for Q2 2016 improved only slightly to 78; from the previous Q1 figure when it dropped seven points to 75 - a similar level to that experienced during one of the country’s worst recessionary climates in 2008/09 - isn’t a surprise. What is interesting though; is that new retail sales data from consumer insights specialist Nielsen presents a far more positive picture of consumer spending realities.

As Nielsen MD Retailer Vertical Africa-Middle East Craig Henry points out; “Despite sentiment currently being worse now than it was in 2008/09; in terms of consumer demand and category sales, including staple foods, as well as from an inflation point of view, we’re actually not worse off.”

In fact, it’s clear that consumption figures were actually far worse in 2008/9 with overall pack sales declining by -7% (staples - 3%; canned food -12%, packaged food -2%; perishables -4%; beverages -8%; personal care -9% and home care -10%) and spend increasing by 5%. This is in stark contrast to the current situation where annual spend is up by 9% and overall pack sales are up by 4%.

Inflation on a Tight Leash

Inflation was also running at more than 12% during 2008/9, whereas it’s currently sitting at 6.2% and is also far more evenly distributed across the income groups. The reason for the containment of inflation is that during the past year to two, retailers and manufacturers have done immense work to restrain price increases, especially on essential food goods, to manage inflation at levels which continue to stimulate sales.

Henry explains; “Manufacturers and retailers have been extremely diligent in trying to ensure that they still bring affordable products to consumers through pricing and promotion strategies as well as affordable packs sizes. This includes strategies like zero rating increases on staples e.g. “same price as last year” promotions - to ensure that consumers can still afford staples like bread.

He adds that as a result, promotion hunting has definitely intensified. “Consumers are more willing to switch brands because of promotions within their store of preference. This is clear when considering their response to the statement “I seldom change stores but actively search for promos” in 2006 31% agreed with this, in 2009 37% and in 2015 it was 36%. (Source: Nielsen Shopper Trends - All Modern Trade Shoppers).

Ship Shape Sales

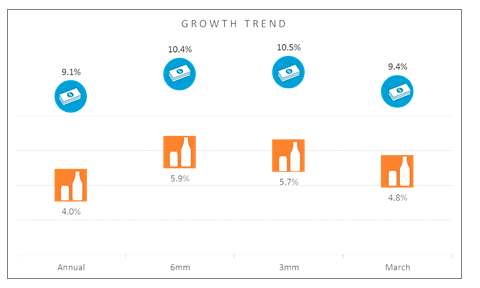

Looking at actual sales trends, Henry says it’s useful to analyse long and short term growth (6- and 3-monthly) versus a year ago. What this reveals is that spend is continuing to increase as consumers implement down-trading strategies.

The above shows that value and pack volume growth has not slowed in the 6-month or 3-month period, due to price increases, inflation or as consumers down traded to smaller packs, which in absolute volume are often more costly than larger packs that offer greater economies of scale. In the shorter term, sales of some agricultural goods have been adversely affected by uncontrollable factors such as the drought e.g. Maize, where inflation has risen to 17.5%.

Category Characteristics

Henry says South Africans may have a more cautionary mindset, but definitely still have a purchasing wallet at present, certain categories have in fact recorded higher than average (9.1%) growth in sales including: Beverages at 14.2% and Confectionery at 10.9% with an accompanying increase in the number of packs sold.

Within the Beverages category consumers have increased their annual consumption (packs) of Carbonated Soft Drinks by 9.6% and 13% by value, while packs of Sports/Energy Drinks have increased by 29.7% (packs) and 27.8% in value. It seems new value alternatives in the market have given this category a boost with lower average pack price levels than last year.

Also within the beverage category, the ‘premiumisation’ of coffee through the introduction of pods and similar offerings has resulted in consumers trading up to smaller quantities, but better quality, coffee. Henry comments; “In tighter economic conditions, you will find people trading back to cheaper coffee but we have also seen the creation of a sub-category that has given rise to a new generation of coffee connoisseurs, with the narrowing of the coffee price differential between pure premium instant vs. pods.”

He adds that because of category innovations like that, it’s important to appreciate that it’s not true that consumers will always trade down to the cheapest product despite their negative sentiment. “The reality is that you don’t have to have a cheaper product in bad times or a premium product in good times but rather a product that meets the ever changing needs of consumers, including through the creation of new or niche category sub sets."

The Sweet Taste of Success

Looking at Confectionery, it’s very much a case of small luxuries definitely still count, so within the chocolate category consumers have shifted from Slabs/Bars to Countlines (single serve offerings) where the cash outlay is considerably less – on avg. R14 p/pack (Slabs) vs R7.50 (Countline).

Henry says that growth in the Chocolate category has also come from product innovation. For example, the premium chocolate brand Lindt that offered high-end slabs has established a new premium, niche category through the introduction of the younger ‘Hello Chocolate’ range. This is still perceived as premium but is more affordable than a larger Lindt chocolate slab.

Another example of this, are the traditional Cadbury’s slabs which have now been complemented by the new Marvellous Creations range that appeals to a younger audience and has proved incredibly popular. “These are great examples of manufacturers appreciating the fact that consumers don’t want to cut back on everything everywhere – they still like to treat themselves but will reconsider cash outlay, pack size and overall product qualities and benefits,” says Henry.

Another insight is that in difficult times snacking is used as a meal alternative. It’s no surprise then that Salty Snacks (Crisps) have grown by 9.8% (units) while biscuits have grown by 8.3% (units). “Perhaps the human insight is that the tighter the squeeze the more consumers revert to less healthy, but cheaper meal substitutes to fill the gap, such as a soda, chips or a chocolate bar!” comments Henry.

Staples Relatively Stable

Looking at a Basket of 20 Staple Categories Nielsen found that there has been a 6.6% value growth and a 0.4% pack decline. The average cost outlay on this basket of staples has risen by R41.80 vs last year (Q1 ‘16 vs Q1’15), now R544 vs R502.22

Within Staples it’s important to note that consumers have cut back actual consumption (packs) on eight of these categories: Sugar, Chicken, Fresh Milk, Canned Pilchards, Tea, Margarine, Toothpaste and Detergents.

Interestingly, consumption of items such as Bread and Chilled Processed Meats have increased as consumers look for cheaper alternatives to eat.

Maize packs have only grown by 2.3% but the cash outlay has increased by a massive 17.5%, due to price increases from the impact of the drought. In Q1 2015, the avg price/pack of maize was R34.27 while in Q1 2016 the avg price/pack is R43.89. This represents an increase of R9.62 (28%), or on average 15% year on year.

The New Retail Reality

What’s clear is that despite South Africans’ apparent pessimism and negative sentiment, they are still spending! What this means is that there is clearly a disconnect between the South African psyche and actual purchase behaviour. As a result, a multi-dimensional approach is required for navigating South Africa’s notoriously ‘schizophrenic’ consumer landscape if a truly deep understanding of the retail reality is to be gained.

Business News Sector Tags: Retail|